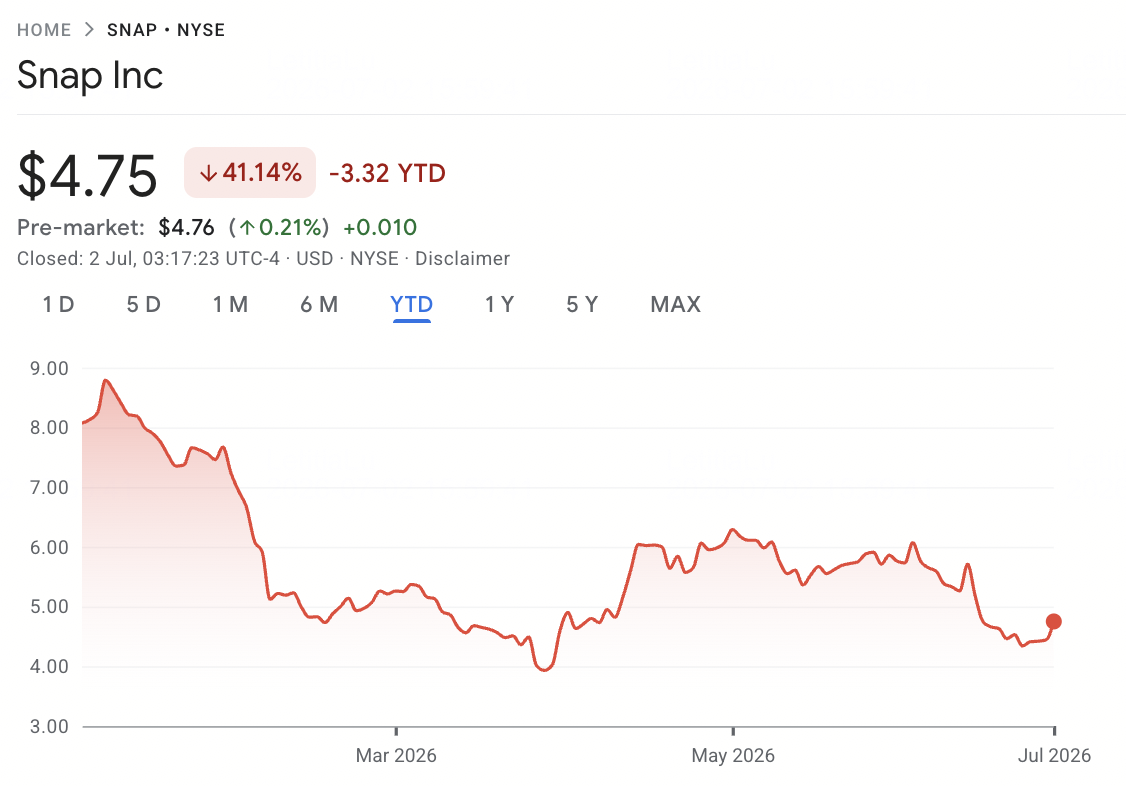

In early July 2026, Snap Inc. (NYSE: SNAP) remains one of the more polarizing names in social media stocks. After entering the year near multi-year highs, SNAP is down more than 40% year to date, weighed down by a collapsed AI partnership, an expensive new hardware bet, and lingering doubts about the company's path to sustained profitability.

The bull case is built on returning daily active user growth, an accelerating advertising business, a credit rating upgrade, and a more than $500 million annualized cost reduction plan tied to the Specs augmented reality launch. The risk is that Snap just walked away from a $400 million AI partnership with Perplexity, is spending heavily on an unproven $2,195 AR headset, and still has not posted a GAAP profit. This guide breaks down the Snap stock forecast, 2026 price scenarios, key risks, and how to trade SNAP stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Snap Traders to Know in 2026

Snap's 2026 story is shaped by a sharp divide between improving core financial metrics and a series of costly, high-risk strategic bets. As Snap navigates a costly hardware bet, a major restructuring, and the loss of a headline AI partnership, market participants must closely track these core structural drivers:

Source: Google Finance

- The Collapsed $400 Million Perplexity Deal: Snap ended its cash-and-equity AI search partnership with Perplexity in the first quarter of 2026, describing the split as amicable. The deal had been expected to contribute meaningfully to 2026 revenue, and its cancellation removed a growth catalyst that had briefly lifted the stock 15% when it was first announced.

- Daily Active Users Returned to Growth: Snapchat's global daily active users rose 5% year over year to 483 million in Q1 2026, adding 9 million users since the prior quarter. Monthly active users also grew 5% to 965 million, helped by Snap Map and Lenses AR filter features.

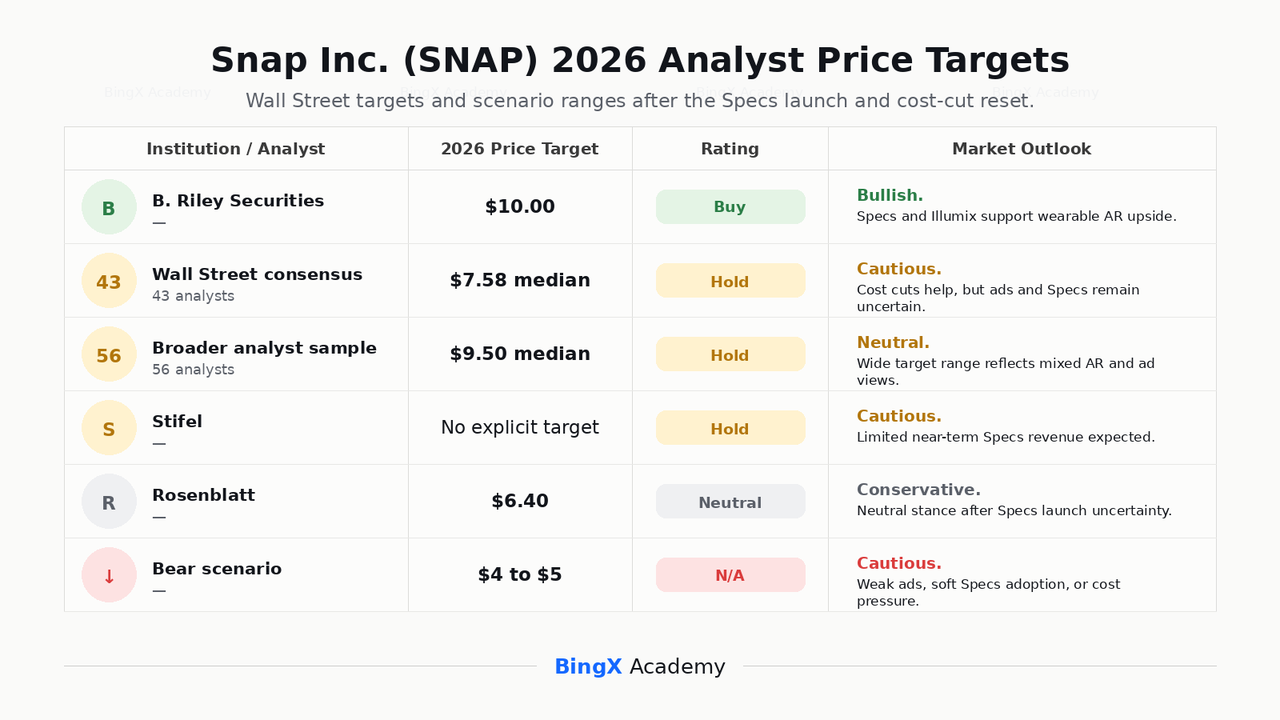

- The $2,195 Specs Launch: Snap unveiled its consumer Specs augmented reality glasses at the Augmented World Expo in June 2026, with pre-orders open and shipments planned for the U.S., U.K., and France starting this fall. The premium price point means near-term unit volume will likely stay low, and Wall Street is split on whether it represents a legitimate long-term hardware franchise, with individual analyst targets ranging from Rosenblatt's cautious $6.40 to B. Riley's bullish $10.00.

- A More Than $500 Million Cost Reduction Plan: Following an April 2026 workforce cut of roughly 16%, or about 1,000 employees, Snap guided to $95 million to $130 million in Q2 restructuring charges as part of a broader plan to remove over $500 million from its annualized cost base starting in the second half of 2026.

- A Credit Upgrade Amid a 40%+ Stock Decline: S&P Global upgraded Snap's credit rating to BB- with a positive outlook in mid-2026, citing 12% Q1 revenue growth and stronger free cash flow. Adjusted EBITDA more than doubled to $233 million and free cash flow reached $286 million in Q1, even as the stock itself remains down more than 40% year to date and well off its 52-week high near $10.41.

What Is Snap Inc. (NYSE: SNAP)?

Snap Inc. (NYSE: SNAP) is a Santa Monica, California-based technology company founded in 2011 by Evan Spiegel, Bobby Murphy, and Reggie Brown. Its flagship product, Snapchat, is a visual messaging application built around a camera-first interface, and the company also builds Spectacles and Specs augmented reality hardware, along with the Bitmoji avatar platform.

Snapchat's app is organized around five core tabs, including Camera, Chat, Snap Map, Stories, and Spotlight, supported by subscription products such as Snapchat+, Lens+, and Snapchat Platinum. The company generates the large majority of its revenue from advertising, including AR ads, Snap ads, story ads, and sponsored snaps, sold primarily to advertisers targeting Snapchat's younger, Gen Z-skewing user base.

In 2026, Snap's biggest strategic shift is its pivot toward augmented reality hardware through Specs, alongside the April 2026 acquisition of spatial AR company Illumix and an expanded partnership with Qualcomm to power future Specs devices with Snapdragon AI chips. Management has framed AR glasses as a long-term bet on a post-smartphone computing era, even as activist investors have pushed the company to consider shrinking or spinning off the AR business.

Read More: Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

Snap's Performance in Early 2026: From Perplexity Collapse to Cost Discipline

Snap entered 2026 carrying momentum from its Perplexity partnership announcement, which had briefly lifted shares 15% when first revealed the prior year. That momentum reversed in the first quarter.

Q1 2026 revenue rose 12% year over year to $1.53 billion, roughly in line with consensus estimates. Adjusted EBITDA more than doubled to $233 million, operating cash flow reached approximately $327 million, and free cash flow nearly tripled to $286 million. Despite these improvements, Snap disclosed that the Iran conflict cost the company an estimated $20 million to $25 million in advertising revenue in March alone, and confirmed that its $400 million Perplexity partnership had ended, with Q2 guidance assuming no contribution from the deal.

Snap Inc. Q1 2026 Financial and Consensus Profile

The Q1 print itself was largely a beat-and-raise setup that the market still sold off, falling roughly 7% in the immediate aftermath, since the in-line Q2 revenue guidance and the confirmed loss of the Perplexity contribution gave investors little reason to raise full-year estimates despite the underlying margin improvement.

|

Metric |

Q1 2026 Result |

Why It Matters |

|

Revenue |

$1.53B |

Up 12% year over year, showing core business growth despite partnership disruption |

|

Net loss |

$89M |

Improved from a $140M loss a year earlier, but GAAP profitability remains unresolved |

|

Adjusted EBITDA |

$233M |

More than doubled year over year, supporting the margin improvement case |

|

Operating cash flow |

$327M |

Shows stronger cash generation from the core business |

|

Free cash flow |

$286M |

Nearly tripled year over year, giving investors a clearer cash-flow recovery signal |

|

Daily active users |

483M |

Up 5% year over year, marking a return to DAU growth |

|

Monthly active users |

956M |

Up 5% year over year, supporting the engagement recovery narrative |

Snap also announced a workforce reduction of approximately 16%, or roughly 1,000 employees, tied to advances in AI-driven efficiency and its push to protect investment in Specs. The company guided Q2 2026 revenue to a range of $1.52 billion to $1.55 billion and flagged $95 million to $130 million in restructuring charges for the quarter, part of a broader plan to cut more than $500 million from its annualized cost base starting in the second half of 2026. Snap's balance sheet remained leveraged, with more than $4.1 billion in long-term debt, but liquid, with over $2.8 billion in cash and short-term investments and a current ratio near 3.5.

Snap's 2026 Trading Strategy: Specs Adoption and Cost Cuts Drive the Setup

Snap's 2026 setup depends on three key signals: whether Specs pre-orders and the fall shipment convert into meaningful revenue, whether the more than $500 million cost reduction plan holds without hurting product execution, and whether advertising revenue growth can keep accelerating without a partner like Perplexity.

- Watch the $4 to $6 Support Zone: After falling more than 40% year to date to a 52-week low near $3.81, SNAP has traded in a rough $4 to $6 range through mid-2026, with a sharp 8%+ rally on July 1 following the credit upgrade and AR product news. A sustained move above $6 would support a retest of higher analyst targets, while a break back below $4 could revive concerns about the pace of the AR spending and advertising softness.

- Cost Discipline vs. Specs Execution Risk: The bull case values Snap's improving free cash flow, expanding margins, and credit upgrade against a backdrop of disciplined restructuring. The risk is that the $2,195 Specs price point limits near-term adoption, and that AR investment continues to weigh on GAAP profitability even as adjusted metrics improve.

- Monitor Advertiser Sentiment and Regulatory Headlines: Snap's advertising business remains sensitive to geopolitical disruptions, as shown by the Iran-related ad revenue hit in March, along with a growing list of regulatory actions, including Australia's teen social media restrictions and state-level lawsuits over youth protections. These headlines can move the stock independent of underlying fundamentals.

The Snap 2026 Forecast: $10+ Specs Upside vs. $4 Advertising Risk Floor

Snap's 2026 outlook depends on whether Specs can build a credible long-term hardware franchise, whether the cost reduction plan translates into a clearer path to GAAP profitability, and whether daily active user growth continues without another partnership setback like Perplexity.

The Bull Case: Specs Adoption and Margin Expansion Push SNAP Above $10

The bull case requires Specs pre-orders to convert into meaningful fall shipment revenue, the more than $500 million cost reduction plan to flow through to margins without disrupting product execution, and daily active user growth to continue accelerating through the back half of 2026. If advertising revenue keeps growing at a low double-digit pace while free cash flow expands, SNAP could move toward the $10 to $16 range implied by the most optimistic analyst targets.

The Base Case: Steady Execution Keeps SNAP Between $6 and $9

The base case assumes disciplined execution without a major new catalyst. Specs ships on schedule but adoption remains modest given the price point, cost cuts proceed roughly as guided, and advertising growth holds in the low double digits. In this scenario, SNAP could consolidate between $6 and $9 as investors wait for clearer evidence that AR hardware can become a meaningful, profitable business line.

Read More: Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

The Bear Case: Advertising Softness or Specs Disappointment Pull SNAP Toward $4

The bear case is driven by slower advertising growth, weak Specs pre-order conversion, higher-than-guided restructuring costs, or renewed geopolitical disruption to ad spending similar to the Iran-related hit in March. If the market shifts back to valuing Snap primarily on its unprofitable GAAP earnings rather than its improving cash flow trajectory, SNAP could retest its 52-week low near $4.

Snap Inc. Price Forecasts for 2026 by Wall Street Analysts

Wall Street remains cautious on Snap after the Perplexity partnership setback, but analysts are still watching whether Specs, cost cuts, and advertising recovery can support a stronger 2026 setup.

|

Institution / Analyst |

2026 Price Target |

Rating |

Market Outlook |

|

B. Riley Securities |

$10.00 |

Buy |

Bullish. Views Specs and the Illumix acquisition as potential drivers for Snap’s wearable AR strategy. |

|

Wall Street consensus |

$7.58 median |

Hold |

Cautious but constructive. Improving cost discipline is offset by uncertainty around ad growth and Specs adoption. |

|

Broader analyst sample |

$9.50 median |

Hold |

Neutral. Reflects a wide range of views on Snap’s advertising recovery and AR hardware execution. |

|

Stifel |

No explicit target cited |

Hold |

Cautious. Expects limited near-term Specs revenue given the high price point and early adoption curve. |

|

Rosenblatt |

$6.40 |

Neutral |

Conservative. Maintains a neutral stance after the Specs launch, citing near-term commercial uncertainty. |

|

Bear scenario |

$4.00 to $5.00 |

N/A |

Cautious. Assumes slower ad growth, weak Specs adoption, or higher restructuring costs. |

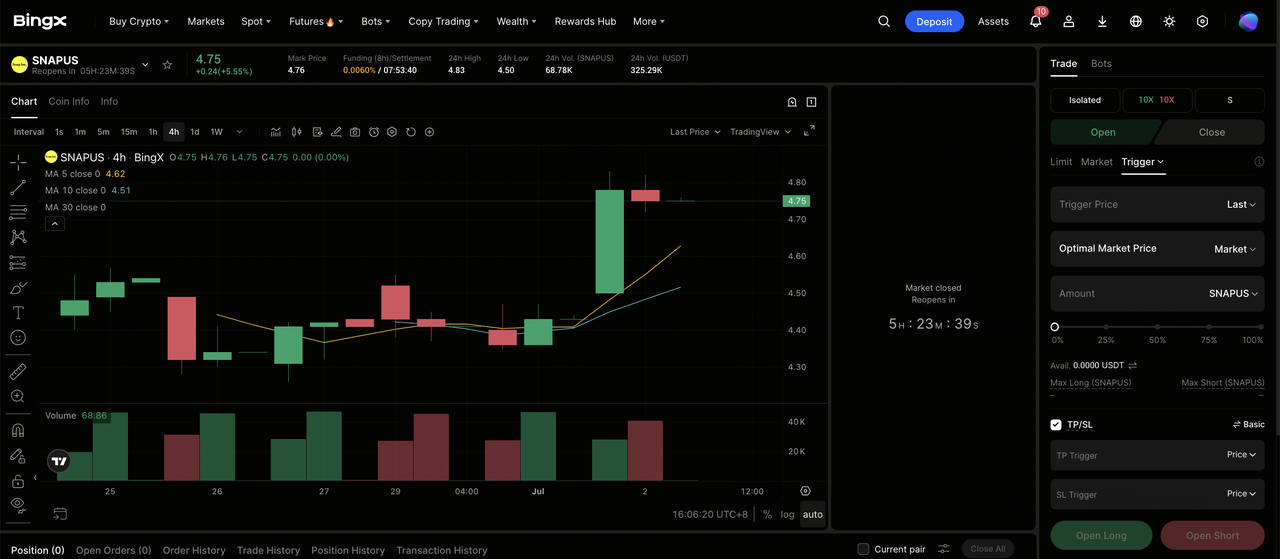

How to Trade Snap Inc. (SNAP) Stock Futures on BingX TradFi

As Snap navigates its highest-stakes product launch to date alongside a major cost restructuring and the fallout from its collapsed Perplexity partnership, tactical traders can capitalize on its sharp bidirectional moves through the BingX TradFi platform.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select Snap Inc. (SNAP). Search for and select the SNAPUS-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect Specs pre-orders to convert into revenue, cost cuts to expand margins, and daily active user growth to continue. Select Open Short if you expect Specs adoption to disappoint, advertising softness to return, or restructuring costs to run higher than guided.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because SNAP has already shown sharp single-day moves in 2026, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. SNAP can react quickly to earnings, Specs shipment updates, regulatory headlines, and advertiser sentiment data.

Top 5 Risks to Consider Before Investing in Snap Inc. Stock

Snap has shown improving cash flow and returning user growth, but SNAP also carries major risks tied to AR execution, advertising cyclicality, competition, and regulatory pressure.

- Specs commercial appeal is unproven: At $2,195, Snap's new AR glasses are priced well above mass-market hardware. Stifel and other analysts expect limited near-term adoption, and the roughly $500 million already invested in AR could take years to generate meaningful returns.

- Snap remains unprofitable on a GAAP basis: Despite improving adjusted EBITDA and free cash flow, Snap posted a net loss of about $89 million in Q1 2026. The company still needs to prove it can reach sustained GAAP profitability, a milestone some analysts previously did not expect until 2028.

- Advertising revenue is exposed to macro and geopolitical shocks: The Iran conflict cost Snap an estimated $20 million to $25 million in ad revenue in March 2026 alone, illustrating how quickly external events can affect its core business.

- Competition from larger platforms is intense: Snap competes directly with Meta's Instagram and other short-form video platforms for both users and advertising dollars, while Meta has also launched its own lower-priced smart glasses, directly challenging Snap's AR strategy.

- Regulatory scrutiny over youth safety is increasing: Snap faces an expanding list of legal and regulatory actions tied to teen users, including state attorney general lawsuits and stricter international rules such as Australia's teen social media restrictions, which could affect user growth and compliance costs.

Final Thoughts: Is Snap Inc. Stock a Buy in 2026?

As of July 2026, Snap Inc. (SNAP) is a company in transition, showing genuine improvement in core financial metrics while making an expensive, high-risk bet on augmented reality hardware. Its return to daily active user growth, more than doubled adjusted EBITDA, nearly tripled free cash flow, and a credit rating upgrade all point to a business tightening its execution. The collapse of the Perplexity partnership and the 16% workforce reduction show that path has not been smooth.

The risk is whether Specs can become a real business rather than a costly experiment, and whether advertising growth can hold up without the AI-driven catalyst Snap had been counting on. After a more than 40% year-to-date decline, SNAP is trading well below its 52-week high near $10.41, and analyst targets remain split between cautious Hold ratings and more optimistic Buy calls tied to the AR opportunity. For traders, SNAP futures on BingX TradFi offer a way to trade around Specs shipment updates, quarterly earnings, and regulatory headlines. For longer-term investors, the key question is whether Snap can convert its restructuring and product bets into sustained, profitable growth.

Related Reading

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?

- Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?

- Qualcomm (QCOM) Stock Price Prediction 2026: Can QCOM Break $260 on Edge AI Growth?

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence