In early July 2026, Ouster, Inc. (Nasdaq: OUST) has emerged as one of the highest-performing names in the "Physical AI" narrative, with the stock up more than 270% over the trailing 12 months and repeatedly setting multi-year highs on the back of Rev8 lidar launches, NVIDIA partnership news, and a wave of infrastructure and defense contract wins.

The bull case is built on 13 consecutive quarters of product revenue growth, the Stereolabs acquisition completing Ouster's transformation into a unified sensing and perception platform, NVIDIA DRIVE Hyperion qualification for Rev8, the removal of key Chinese competitor Hesai from U.S. federal procurement under NDAA Section 164, a 700-plus BlueCity site deployment footprint, and management's stated path to profitability by 2027.

The risk is that OUST already trades at roughly 9x 2026 estimated revenue, remains adjusted EBITDA-negative, has diluted shareholders through a $97.5 million follow-on raise, and remains highly sensitive to speculative Physical AI sentiment. This guide breaks down the Ouster stock forecast, 2026 price scenarios, key risks, and how to trade OUST stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Ouster Traders to Know in 2026

Ouster's 2026 story is shaped by a rare combination of strong product execution, a fortuitous regulatory tailwind, and a valuation that has already priced in a lot of the Physical AI narrative. As OUST navigates the transition from lidar sensor supplier to full-stack perception platform, market participants must closely track these core structural drivers:

- 13 Consecutive Quarters of Product Revenue Growth: Ouster's Q1 2026 revenue of $49.0 million was up 49% year over year, the 13th consecutive quarter of product revenue growth, with lidar unit shipments hitting a record 8,300 sensors and total sensor shipments, including Stereolabs cameras, exceeding 12,600 units.

- The Rev8 Native Color Lidar Launch and NVIDIA Qualification: Ouster launched the Rev8 OS family in Q1 2026, described by the company as the world's first native color lidar, with 2x range and resolution improvements. In May 2026, Rev8 was qualified for the NVIDIA DRIVE Hyperion Level 4 autonomous vehicle reference platform, opening a direct path to global automotive customers.

- NDAA Section 164 Bans Hesai from U.S. Federal Procurement: Effective after June 2026, NDAA Section 164 removes key Chinese competitor Hesai from U.S. federal procurement, positioning Ouster as the primary U.S.-aligned, at-scale lidar platform for defense and Department of Transportation-funded infrastructure work.

- The Stereolabs Acquisition Adds Cameras and 10,000+ Customers: Ouster closed its acquisition of Stereolabs on February 4, 2026, adding AI vision, over 90,000 shipped ZED cameras, more than 10,000 customers, and an EBITDA-positive business that broadens Ouster's addressable market beyond lidar into unified perception hardware and software.

- BlueCity Deployment for the 2026 FIFA World Cup: Ouster's BlueCity smart infrastructure product was deployed at more than 40 locations on highways around MetLife Stadium ahead of the July 19, 2026 FIFA World Cup final, part of a broader footprint of over 700 contracted BlueCity sites globally.

Read More: Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

What Is Ouster, Inc. (Nasdaq: OUST)?

Ouster, Inc. (Nasdaq: OUST) is a San Francisco, California-based sensing and perception company founded in 2015 and led by CEO Angus Pacala. The company designs and manufactures high-resolution digital lidar sensors used across four core end markets, automotive, industrial, robotics, and smart infrastructure, and, following the February 2026 Stereolabs acquisition, has expanded into cameras, sensor fusion, and perception software as a unified Physical AI platform.

Ouster's product portfolio spans three main sensor categories. The Outer Sensor (OS) family includes OSDome for hemispheric field of view, OS0 for wide view, OS1 for mid-range, and OS2 for long-range, joined in 2026 by the Rev8 OS flagship with 256 channels, up to 500 meters of range, and native color sensing. The DF series covers solid-state digital lidar for advanced driver assistance systems and autonomous driving. The Velodyne line, added through the 2023 acquisition, includes VLP-16, VLP-32, and VLS-128 surround-view sensors. Ouster Gemini and BlueCity extend the platform into smart infrastructure, traffic operations, and safety monitoring, while ZED cameras from Stereolabs cover AI vision and 3D depth perception.

In 2026, Ouster's biggest strategic shift is its repositioning from a lidar hardware vendor to a vertically integrated Physical AI platform combining digital lidar, cameras, AI compute, sensor fusion, and perception software. Management has framed this as a way to lock in workflow-level customer commitments across industrial, robotics, and infrastructure markets, rather than competing purely on lidar hardware specifications.

Read More: Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

Ouster’s Performance in Early 2026: Growth With Profitability Still Ahead

Ouster entered 2026 with strong operating momentum. Q1 revenue reached $49.0 million, up 49% year over year, while product revenue grew 55%. GAAP gross margin expanded to 43%, and the company ended the quarter with about $175 million in cash and short-term investments and no debt.

The weaker point was profitability. Adjusted EBITDA loss remained around $7 million, excluding acquisition and integration charges, while GAAP EPS missed consensus as Stereolabs integration costs weighed on results. Management is still targeting profitability in 2027, which means investors are paying for future execution rather than current earnings power.

Ouster, Inc. Q1 2026 Financial and Consensus Profile

|

Metric |

Q1 2026 Result |

Why It Matters |

|

Revenue |

$49.0 million |

Up 49% year over year |

|

Sensor shipments |

12,600+ |

Includes lidar and Stereolabs cameras |

|

GAAP gross margin |

43% |

Shows improving product economics |

|

Adjusted EBITDA |

About -$7 million |

Losses are narrowing but still negative |

|

Cash and short-term investments |

About $175 million |

Provides runway for integration and growth |

|

Q2 revenue guidance |

$49.5 million to $52.5 million |

Next key checkpoint for growth consistency |

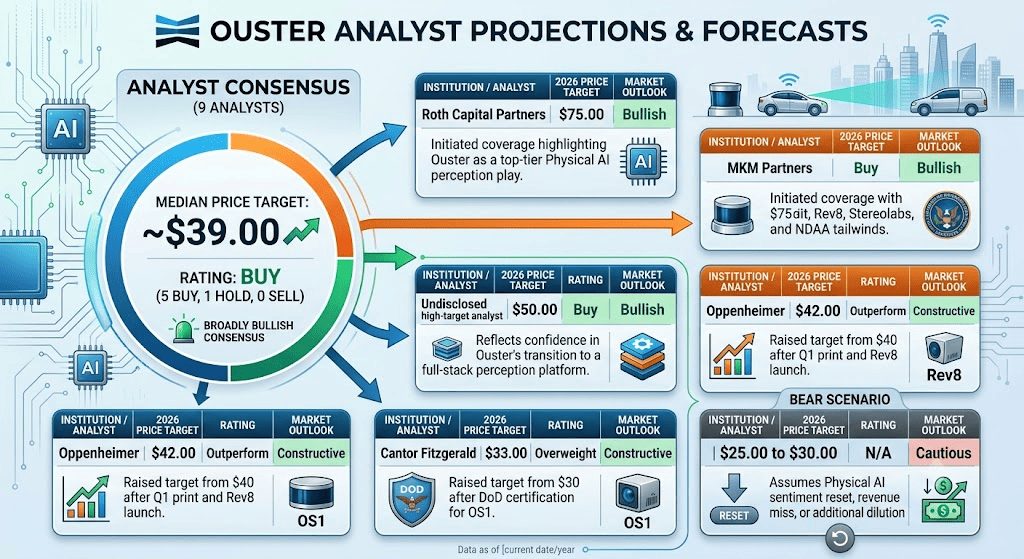

Following the Q1 print and Rev8 launch, analysts became more constructive. Oppenheimer raised its target to $42, Cantor Fitzgerald moved to $33, and Roth Capital Partners and MKM Partners initiated coverage with $75 targets. The next major checkpoint is Ouster’s Q2 earnings report, where investors will watch revenue guidance, gross margin, bookings, and progress toward 2027 profitability.

Read More: Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

Ouster's 2026 Trading Strategy: Rev8 Ramp and Regulatory Tailwinds Drive the Setup

Ouster's 2026 setup depends on three key signals: whether Rev8 adoption scales across NVIDIA DRIVE Hyperion customers and industrial partners, whether the removal of Hesai from U.S. federal procurement translates into large infrastructure and defense wins, and whether the Stereolabs integration accelerates the path to adjusted EBITDA profitability.

- Watch the $40 to $50 Consolidation Zone: After surging to multi-year highs above $60 in mid-May 2026 on the NVIDIA DRIVE Hyperion news, OUST has consolidated in a broad $40 to $50 range through early July. A sustained move above $55 would support a retest of the $60-plus highs, while a break back below $35 could revive concerns about dilution and valuation.

- Physical AI Tailwinds vs. Valuation Risk: The bull case values Ouster as the only U.S.-aligned, at-scale perception platform for Physical AI, backed by NVIDIA DRIVE Hyperion qualification, DoD certification, and Hesai's exit from U.S. federal work. The cautious case is that OUST already trades near 9x 2026 estimated revenue, ahead of many high-growth defense and industrial peers.

- Monitor Bookings and Insider Activity: OUST is highly sensitive to contract announcements, from BlueCity DOT wins to ARGUS counter-drone and AIM Intelligent Machines partnerships. Insider activity has also been notable, with co-founder Mark Frichtl filing multiple intent-to-sell forms totaling more than 190,000 shares over recent months, while overall insider selling outpaced buying by roughly $2.5 million over the trailing 12 months.

Read More: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

The Ouster 2026 Forecast: $75 Physical AI Upside vs. $30 Execution Risk Floor

Ouster's 2026 outlook depends on whether the Physical AI narrative sustains through the second half of the year, whether Rev8 and Stereolabs integrations translate into higher-margin recurring revenue, and whether the company can meet its stated 2027 profitability target without additional large equity raises.

The Bull Case: Rev8 Adoption and Hesai Void Push OUST Above $75

The bull case requires Rev8 to translate NVIDIA DRIVE Hyperion qualification into design wins with global automakers, BlueCity to expand its 700-plus deployment footprint into more large state DOT and federal infrastructure programs, and the Stereolabs integration to reach EBITDA profitability faster than the 2027 target. Combined with Hesai's removal from U.S. federal procurement and continued DoD-linked defense demand, this could push OUST toward the $75 targets from Roth Capital and MKM Partners.

The Base Case: Steady Execution Keeps OUST Between $40 and $55

The base case assumes disciplined execution without a major new re-rating catalyst. Ouster hits the top end of its $49.5 million to $52.5 million Q2 revenue guidance, gross margin holds in the low 40% range, and BlueCity and industrial wins continue at a steady pace. In this scenario, OUST could consolidate between $40 and $55 as investors wait for Q3 to confirm the path toward the 2027 profitability target.

The Bear Case: Physical AI Sentiment Reset Pulls OUST Toward $30

The bear case is driven by a broader unwind in the Physical AI narrative, a revenue miss, further dilution beyond the May 2026 $97.5 million follow-on, or a slower-than-expected Rev8 automotive adoption cycle. If the market shifts back to valuing Ouster on current cash flow rather than long-dated Physical AI upside, OUST could retest the $25 to $30 range, closer to Cantor Fitzgerald's original target zone.

Ouster Inc. Price Forecasts for 2026 by Wall Street Analysts

Wall Street remains broadly constructive on Ouster, but analyst targets are widely spread because the company sits between strong growth momentum and still-negative profitability.

|

Institution / Analyst |

2026 Price Target |

Rating |

Market Outlook |

|

Roth Capital Partners |

$75.00 |

Buy |

Bullish. Initiated coverage highlighting Ouster as a top-tier Physical AI perception play. |

|

MKM Partners |

$75.00 |

Buy |

Bullish. Initiated coverage with the same $75 target, citing Rev8, Stereolabs, and NDAA tailwinds. |

|

Undisclosed high-target analyst |

$50.00 |

Buy |

Bullish. Reflects confidence in Ouster's transition to a full-stack perception platform. |

|

Oppenheimer |

$42.00 |

Outperform |

Constructive. Raised target from $40 after Q1 print and Rev8 launch. |

|

Wall Street consensus (9 analysts) |

~$39.00 median |

Buy |

Broadly bullish. 5 Buy, 1 Hold, 0 Sell, with targets ranging from $33 to $75. |

|

Cantor Fitzgerald |

$33.00 |

Overweight |

Constructive. Raised target from $30 after DoD certification for OS1. |

|

Bear scenario |

$25.00 to $30.00 |

N/A |

Cautious. Assumes Physical AI sentiment reset, revenue miss, or additional dilution. |

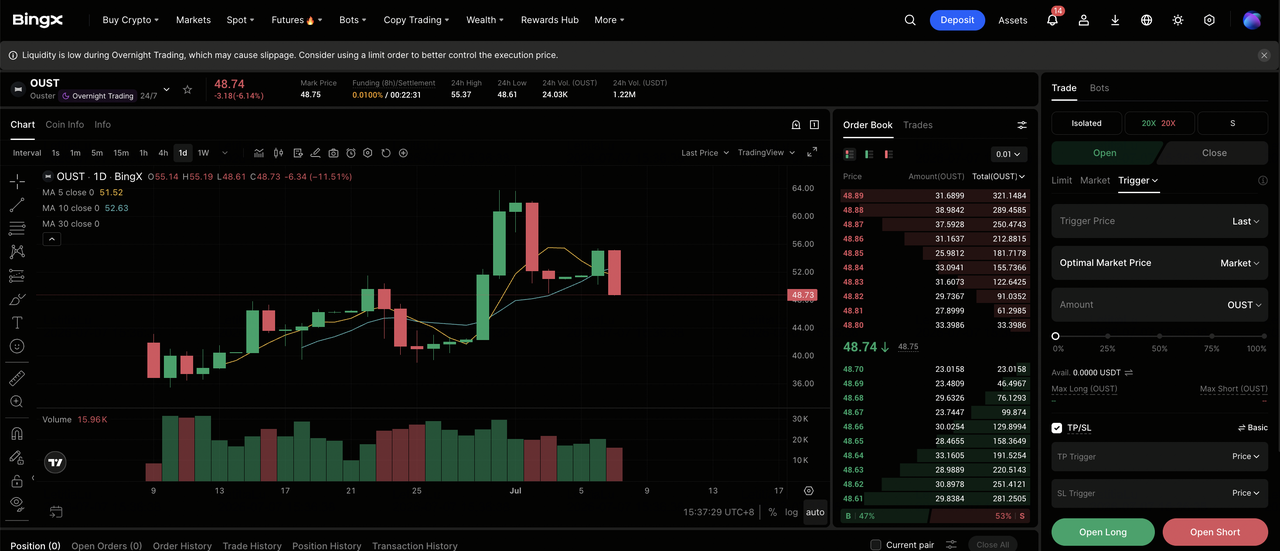

How to Trade Ouster (OUST) Stock Futures on BingX TradFi

As Ouster navigates the Rev8 ramp, NVIDIA DRIVE Hyperion adoption, NDAA-driven federal procurement wins, and the Stereolabs integration, tactical traders can capitalize on its sharp bidirectional moves through the BingX TradFi platform.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select Ouster (OUST). Search for and select the OUST-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect Rev8 automotive design wins, federal infrastructure and defense contracts, and a clean path to 2027 profitability. Select Open Short if you expect a Physical AI sentiment reset, revenue miss, or additional dilution.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because OUST has already shown 14% single-session moves in 2026, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. OUST can react quickly to earnings, NVIDIA-related headlines, federal procurement announcements, and Physical AI-linked sector sentiment.

Top 5 Risks to Consider Before Investing in Ouster Stock

Ouster has one of the more compelling operational and regulatory setups among small-cap lidar and Physical AI names, but OUST also carries major risks tied to valuation, dilution, insider activity, execution, and sentiment cyclicality.

- Valuation is stretched after the 2026 rally: OUST trades at roughly 9x 2026 estimated revenue after rallying more than 270% over the trailing 12 months, in line with high-growth defense and AI peers. Multiple compression could be sharp if execution disappoints or Physical AI enthusiasm fades.

- Adjusted EBITDA remains negative: Despite 49% revenue growth and expanding gross margin, Ouster's adjusted EBITDA loss was about $7 million in Q1 2026, and management's stated profitability target is 2027 rather than 2026, leaving meaningful room for execution risk.

- Dilution history continues: Ouster raised approximately $97.5 million in a follow-on equity offering in May 2026, adding to a multi-year history of shareholder dilution. Further capital raises are possible if the path to profitability slips.

- Insider selling has been persistent: Co-founder Mark Frichtl has filed multiple intent-to-sell forms totaling more than 190,000 shares over recent months, and total insider selling has outpaced buying by roughly $2.5 million over the trailing 12 months, which can weigh on sentiment.

- Physical AI sentiment is highly cyclical: OUST's price action has closely tracked the Physical AI theme, which is inherently narrative-driven. A broader unwind in AI-linked speculative themes, or a rotation away from small-cap sensor makers, could pressure the stock even if underlying fundamentals stay intact.

Final Thoughts: Is Ouster Stock a Buy in 2026?

As of July 2026, Ouster, Inc. (OUST) is one of the strongest-executing names at the intersection of digital lidar, Physical AI, and U.S.-aligned sensor supply chains. Its 13 consecutive quarters of product revenue growth, Rev8 native color lidar launch, NVIDIA DRIVE Hyperion qualification, Stereolabs acquisition, NDAA Section 164 tailwind, and 700-plus BlueCity smart infrastructure deployment footprint together support the argument that Ouster has moved beyond the lidar hardware category into a broader perception platform.

The risk is that a lot of that story is already reflected in the stock, with OUST up more than 270% year over year and trading at roughly 9x 2026 estimated revenue. Analyst targets remain broadly bullish but widely dispersed, from Cantor Fitzgerald's $33 on the cautious side to Roth Capital and MKM's $75 on the aggressive side, with the consensus clustered near $39. For traders, OUST futures on BingX TradFi offer a way to trade around Q2 earnings, NVIDIA-related headlines, federal infrastructure wins, and Physical AI sentiment cycles. For longer-term investors, the key question is whether Ouster can convert its Rev8 momentum, NVIDIA qualification, and Hesai-free U.S. federal opportunity into sustained, profitable growth by 2027 without further material dilution.

Related Reading

- Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?