In April 2026, UnitedHealth Group (UNH) is navigating a critical reset year. After a bruising 12-month period that saw the stock shed nearly 46% of its value, the diversified healthcare giant is pivot-pointing toward a technology-led recovery. While the stock has struggled with a 13% year-to-date decline to $306.91, institutional sentiment is shifting.

Bulls point to a surprise 2.48% CMS rate hike and a $1.6 billion investment in generative AI as catalysts for a massive valuation re-rating. Conversely, skeptics remain wary of a pending Department of Justice (DOJ) probe and the lingering impact of 2025 pricing missteps that compressed earnings.

As the April 21, 2026, earnings report approaches, UNH is evolving beyond a traditional insurer. With the rollout of Avery, its generative AI companion, and a national expansion of doula support services, UNH is weaponizing its Optum data engine to automate claims and reduce operating costs by $1 billion. This guide breaks down the UNH stock price prediction for 2026 using data from UBS, Raymond James, Zacks Research, and Simply Wall St.

You will also discover how to gain exposure to UnitedHealth (UNH) through UNHON, the Ondo tokenized stock available on the BingX Spot Market.

Top 5 Things for UnitedHealth Investors to Know in 2026

Before diving into the detailed price targets, it is essential to understand the core operational shifts and regulatory catalysts that are currently defining UnitedHealth's trajectory for the 2026 fiscal year.

- The $1.6B AI Offensive: UNH has earmarked $1.6 billion for AI and automation in 2026, specifically targeting Optum margin recovery and a $1 billion reduction in G&A expenses.

- The CMS Relief Rally: A surprise decision by CMS to raise 2027 Medicare Advantage payments by 2.48% (vs. a feared 0.09%) has effectively removed a major regulatory black swan risk for the medium term.

- Billionaire Accumulation: Paul Tudor Jones increased his fund's stake in UNH by over 13,000% in recent filings, signaling that elite investors view the current 13.5x forward P/E as a generational entry point.

- The Q1 Earnings Hurdle: Analysts expect a 10% YoY decline in EPS to $6.45 for the April 21 release, making management’s full-year guidance of $17.75+ the ultimate make-or-break metric for 2026.

- Tokenized Accessibility: Through Ondo Finance, investors can now trade UnitedHealth tokenized stock UNHON on BingX, allowing Web3 users to access UNH stock yields and price action on-chain via blockchain-based tokenized securities.

What Is UnitedHealth Group (UNH)?

UnitedHealth Group is the largest healthcare company in the world by revenue, projected to hit $440 billion in 2026. The company operates through two distinct yet complementary pillars: UnitedHealthcare, which provides insurance coverage to millions, and Optum, a massive health services platform spanning pharmacy benefits (OptumRx), clinical care (Optum Health), and data analytics (Optum Insight).

Under the leadership of CEO Andrew Witty, UNH has built a vertically integrated flywheel where data from insurance claims informs care delivery, theoretically lowering costs and improving outcomes. Despite recent self-inflicted operational issues, the company maintains a robust dividend yield of 3.2% and a dominant market share in the lucrative Medicare Advantage segment.

UnitedHeatlh (UNH) Stock Performance in 2025: A Review

UnitedHealth Group (UNH) endured a significant reset year in 2025, with shares plummeting approximately 35% to 46% as the company grappled with a series of operational and regulatory headwinds. The stock's primary distress stemmed from a notable earnings miss in the first quarter of 2025, where management admitted to misjudging customer premium pricing and underestimating medical utilization costs.

This execution misstep was compounded by a high-profile CEO transition in May 2025 and the confirmation of a U.S. Department of Justice antitrust probe in July, leading investors to trade the stock at multiples typically reserved for low-growth utilities rather than a premier healthcare innovator.

UnitedHealth’s 2026 Strategy: The Margin Repair

- Project Avery: The national rollout of a generative AI assistant designed to streamline provider workflows and automate 20% of routine claim processing by year-end.

- Medicare Advantage Right-Sizing: After underpricing premiums in 2025, UNH is exiting underperforming markets and repricing bids for 2027 to ensure a return to historical margin targets.

- Maternal Health Push: The March 2026 launch of national Doula Support services aims to reduce high-cost birth complications like C-sections and preterm births for 7.2 million members.

UnitedHealth Stock Investment Outlook 2026: $410 Recovery vs. $245 Regulatory Risk

UnitedHealth stock forecasts for 2026 by various analysts

The 2026 outlook for UNH stock is a tug-of-war between its massive cash flow generation and the political pressures of an election-cycle regulatory crackdown.

The Bull Case: UnitedHealth’s $410 Blue Chip Rebound

The bullish narrative is anchored in a massive valuation mean-reversion, driven by the decoupling of UNH’s stock price from its fundamental earnings power. Historically, UNH has commanded a 20x–25x premium multiple, yet it currently languishes at a forward P/E of roughly 13.5x, a tier usually reserved for stagnant utilities. If the April 21 earnings call confirms that the first-quarter Medical Loss Ratio (MLR) has stabilized in the low-to-mid 85% range, it will signal that the 2025 pricing missteps are fully rectified. UBS maintains a high-end $410 price target, banking on the 65/35 first-half earnings split to front-load a recovery that markets haven't yet priced in.

Insightfully, the alpha in this scenario comes from the $1.6 billion AI multiplier. Beyond simple automation, the rollout of Avery is expected to yield $1 billion in immediate G&A cost reductions for FY 2026. If management demonstrates that AI is successfully offsetting the 7% medical cost inflation trend, UNH will likely capture the 19%–30% upside projected by Raymond James and consensus analysts. For traders, this scenario transforms UNH from a value trap into a high-octane recovery play, where the combination of the 3.2% dividend yield and a P/E re-rating toward 18x creates a compelling total return profile.

The Base Case: UNH Stock’s $335 Fair Value Consolidation

The base case positions UNH as a steady-as-she-goes compounder, where the stock reaches a mean analyst target of $335 through cautious consolidation. The recent 2.48% CMS reimbursement hike acts as a definitive valuation floor, effectively neutralizing the worst-case regulatory fears for Medicare Advantage. While revenue is projected to track near $440 billion, the stock may face temporary resistance as it absorbs the technical back-end loaded nature of the OptumRx and Optum Insight segments. In this scenario, investors are paid to wait, capturing a 3.2% dividend while the company executes its phased national rollout of new clinical offerings like the Doula Support initiative.

Practically, this outlook assumes a soft landing for the healthcare giant. While the DOJ probe remains a headline distraction, its impact is mitigated by UNH’s sheer scale and the 9% projected growth in Optum Health. Trading will likely remain range-bound between $300 and $340 until Q3, when the Avery AI tools move from pilot to full production. For the patient investor, this represents a low-volatility entry point where the forward P/E gradually drifts toward a fair-value estimate of 16x, delivering a reliable 10%–15% capital appreciation by year-end.

The Bear Case: UNH Stock at $245 Amid DOJ Contagion

The bear case is triggered by a triple threat of regulatory litigation, margin compression, and macro-headwinds. If the DOJ’s antitrust investigation moves toward a formal challenge of the Optum-UnitedHealthcare vertical integration, the Dimon-like premium on UNH’s stock would evaporate. This narrative gains momentum if Q1 results reveal that healthcare spending remains stubbornly high, with an MLR exceeding 86%, indicating that premium hikes are failing to keep pace with clinical utilization. In this high-risk environment, a failure to meet the $17.75 adjusted EPS guidance would force a mass exodus of institutional flight-to-quality capital.

Under this pressure, the stock would likely breach its $280 support level and test the $245 floor, a level not seen in years. The catalyst for this downward spiral would be multiple contagion, where investors stop treating UNH as a tech-enabled innovator and begin pricing it as a pure-play insurer exposed to the whims of the Trump administration's crackdowns. If medical cost inflation sustains above 7% and AI efficiency gains fail to materialize by mid-2026, the stock’s dividend yield which sits currently at 3.2% may become the only remaining support for a franchise struggling to prove its structural moat is still intact.

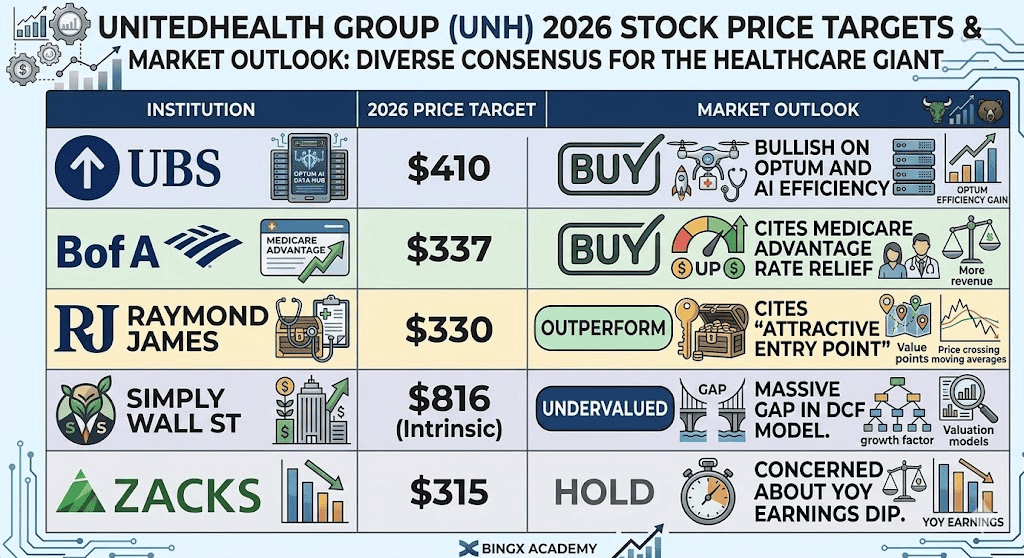

UnitedHealth (UNH) Stock Price Forecasts for 2026

|

Institution |

2026 Price Target |

Market Outlook |

|

UBS |

$410 |

Buy: Bullish on Optum and AI efficiency. |

|

BofA |

$337 |

Buy: Cites Medicare Advantage rate relief. |

|

Raymond James |

$330 |

Outperform: Cites "attractive entry point." |

|

Simply Wall St |

$816 (Intrinsic) |

Undervalued: Massive gap in DCF model. |

|

Zacks Research |

$315 |

Hold: Concerned about YOY earnings dip. |

How to Trade UnitedHealth (UNH) on BingX

You can now gain exposure to the world’s largest healthcare provider via the blockchain using BingX AI predictive tools to optimize your entry points. BingX offers UNHON, a tokenized version of UNH stock provided by Ondo Finance, which allows users to trade institutional-grade assets with the efficiency of the Ondo ecosystem.

Buy, Sell, or HODL UNHON Ondo Tokenized UnitedHealth Stock on Spot Market

UNHON/USDT trading pair on BingX spot market

- Navigate to BingX Spot Market.

- Search for the UNHON/USDT pair.

- Execute a Buy order to hold the tokenized stock and benefit from UNH price appreciation and dividends.

Top 5 Risks to Watch for UNH Investors in 2026

To successfully navigate the 2026 healthcare market, investors must balance UnitedHealth’s AI-driven efficiency gains against a complex landscape of regulatory probes, medical cost inflation, and shifting government reimbursement policies.

- DOJ Antitrust Probe: Any move to force a divestiture of Optum from UnitedHealthcare would dismantle the company’s vertical integration strategy.

- Medical Cost Ratio (MLR) Volatility: If post-pandemic care utilization remains elevated, 2026 margins will continue to suffer.

- Political Rhetoric: As a mega-insurer, UnitedHealth is a frequent target for both parties during election cycles regarding drug pricing and excessive profits.

- AI Execution Risk: If the $1.6 billion AI investment fails to yield the $1 billion in projected savings, the stock’s premium valuation may never return.

- Cybersecurity: Following previous sector-wide breaches, UNH remains a high-value target for ransomware, which could disrupt claims processing.

Final Thoughts: Should You Invest in UnitedHealth (UNH) Stock in 2026?

UnitedHealth in 2026 is a classic contrarian play. While the headlines are dominated by regulatory probes and earnings dips, the underlying fundamentals, $440 billion in revenue and a $1.6 billion AI bet, suggest a company that is simply too large and too integrated to stay down. For long-term investors, the current discount relative to historical P/E multiples offers a rare opportunity to buy a fortress healthcare asset at utility prices.

Risk Reminder: Trading tokenized stocks like UNHON or equities like UNH involves significant risk. Healthcare stocks are highly sensitive to government policy and interest rate shifts. Always perform your own due diligence before investing.

Related Reading

- Johnson & Johnson (JNJ) Stock Price Prediction 2026: Oncology Velocity or $15B Talc Trap?

- JPMorgan Chase (JPM) Price Prediction 2026: Fortress Defense or AI-Driven Alpha at $330?

- Goldman Sachs (GS) Price Prediction 2026: Strategic Renaissance or Value Trap at $860?

- GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?