At the start of 2026, Intel (INTC) was no longer the struggling giant of 2024. Under the disciplined leadership of CEO Lip-Bu Tan, the company successfully executed its "5 nodes in 4 years" roadmap, bringing the 18A (1.8nm) process into high-volume manufacturing. However, the market remains split: while high-profile institutional buyers like APG Asset Management and Allianz SE have aggressively increased their stakes, the foundry division still reported a $2.5 billion loss in the most recent quarter.

The Intel stock forecast for 2026 is defined by two competing narratives:

• the Manufacturing Reality that Intel is reclaiming the transistor lead, and

• the Financial Reality that building a world-class foundry is an incredibly capital-intensive cash incinerator that won't break even until 2027.

For traders, this creates a high-beta environment where every yield update from the 18A node triggers double-digit volatility.

This guide breaks down the INTC price prediction for 2026 using real-time data from Tigress Financial, Goldman Sachs, and TIKR, alongside analysis of the $89 valuation model. You will also learn how to trade these moves using USDT-margined INTC stock perpetuals on BingX TradFi.

5 Key Highlights for Intel Investors in March 2026

• 18A Momentum: Intel’s 18A process is reportedly weeks ahead of TSMC’s 2nm chips, powering the new Core Ultra Series 3 (Panther Lake) AI PCs.

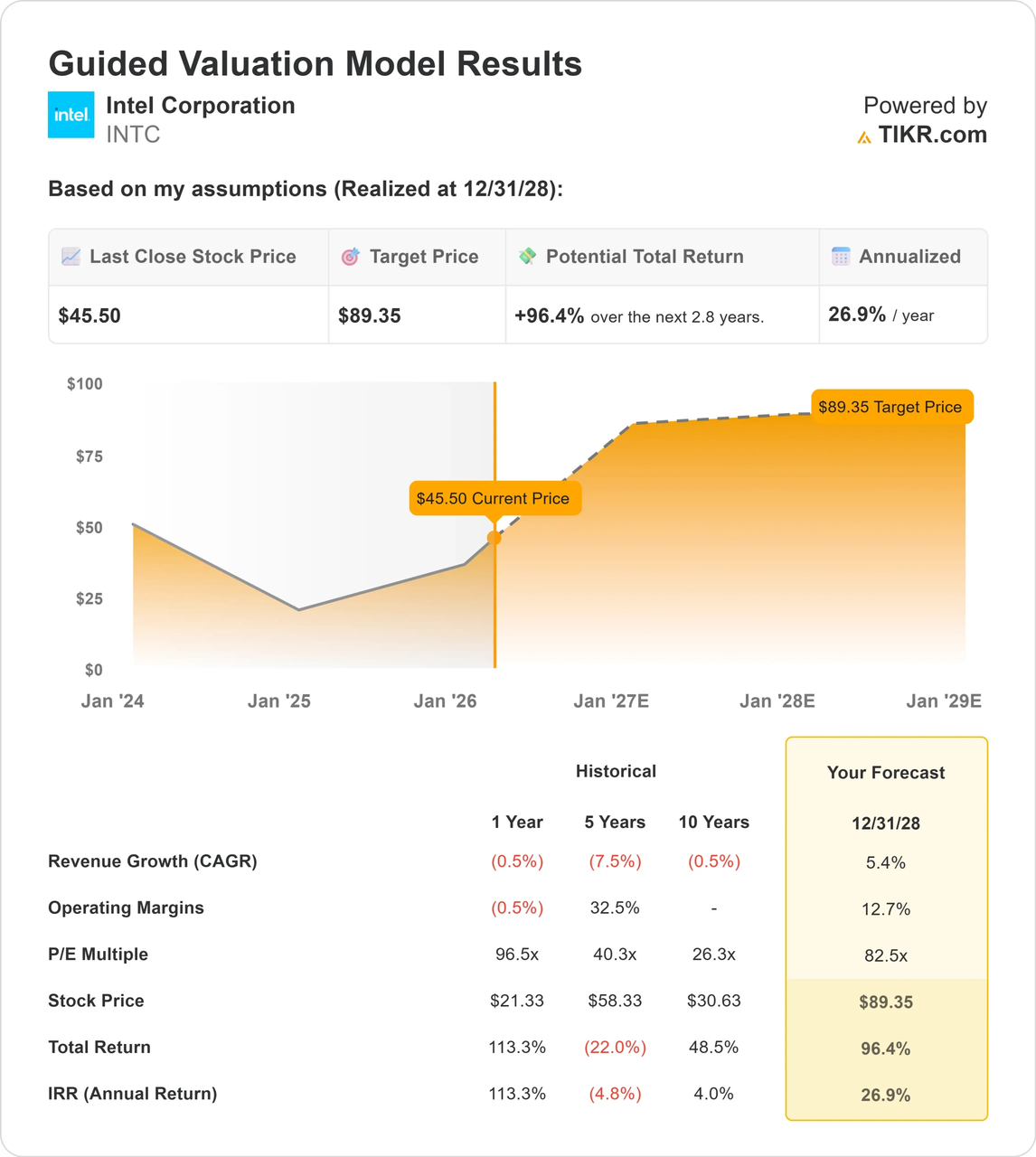

• The $89 Target: TIKR’s guided valuation model suggests a 96.4% upside from current levels, provided operating margins recover to 12.7%.

• Foundry Independence: Intel has spun off its Foundry unit into a standalone subsidiary, a move designed to court frenemies like Nvidia and Microsoft for 2028 production.

• Institutional Tug-of-War: While 64.5% of Intel is owned by institutions, recent 13F filings show a rotation; value funds are buying the turnaround while growth funds wait for margin expansion.

• Geopolitical Hedge: Intel is increasingly viewed as a National Champion, with significant U.S. government backing making it a strategic hedge against any potential Taiwan Strait supply chain disruptions.

What Is Intel (INTC) Stock?

Intel is a Santa Clara-based semiconductor pioneer that designs and manufactures microprocessors for the global personal computer and data center markets. Unlike fabless rivals like AMD or NVIDIA, Intel is an Integrated Device Manufacturer (IDM), meaning it owns and operates its own silicon wafer factories (fabs).

In 2026, Intel’s value proposition has shifted. It is no longer just a CPU company; it is a Systems Foundry. By opening its factories to external customers, Intel aims to become the Western alternative to TSMC. The Success or Failure of 2026 hinges on yield rates, the percentage of functional chips produced per wafer.

Intel vs. NVIDIA: Which Semiconductor Stock Should You Trade in 2026?

While both Intel and NVIDIA are pivotal to the AI revolution, they occupy opposite ends of the supply chain in 2026. On BingX, selecting the right perpetual depends on whether you are betting on the foundry infrastructure or the AI compute dominance:

| Feature | Intel (INTC) | NVIDIA (NVDA) |

| Business Model | IDM (Manufacturing + Foundry) | Fabless (Design Leader, uses TSMC/Intel) |

| 2026 Context | High Capex; Turnaround play | Market Leader; Growth Sustainability play |

| Primary Driver | 18A Node Yields & Fab Utilization | Blackwell/Rubin GPU Demand & CUDA Moat |

| Volatility Profile | Extreme; tied to manufacturing milestones | High; tied to AI CapEx and earnings beats |

Practical Tip: In 2026, INTC is the superior instrument for trading U.S. semiconductor onshoring and the success of the Systems Foundry model. NVIDIA remains the preferred choice for those looking for direct exposure to global AI infrastructure spending and the software-hardware ecosystem lead.

Intel 2026 Outlook: The EBITDA Ramp vs. The Margin Squeeze

Historically, Intel’s stock follows its manufacturing tick-tock cycle. The 2026 forecast is a battle between current losses and future earnings power.

• The Bearish Baseline: The foundry business remains a drag on the balance sheet, with negative free cash flow projected through part of 2026 as Intel builds out its New Mexico and Ohio mega-fabs.

• The Bullish Pivot: Analysts expect a massive EBITDA ramp-up, potentially growing from $1.2 billion in 2024 to $25.1 billion by 2028. If Intel hits its 2026 EPS target of $0.48, it validates INTC stock's U-shaped recovery.

Intel (INTC) stock price prediction by TIKR

Intel Stock Price Forecasts for 2026: Bull vs. Bear Outlook

| Source/Institution | 2026 Price Target | Market Outlook |

| Tigress Financial | $66.00 | Bullish: Multi-year upside from AI PC leadership. |

| TIKR Model | $89.35 | Super-Bullish: Based on 12.7% operating margins. |

| UBS | $49.00 | Neutral: Cautious on foundry execution risks. |

| Simply Wall St (DCF) | $33.03 | Bearish: Suggests stock is at a 39% premium to cash flow. |

| Wedbush | $30.00 | Strong Bear: Concerned about AMD’s server share gains. |

The Bull Case: The 18A Golden Cross to $80+

The bull narrative centers on Product Leadership. If Intel’s 18A yields hit 75% by mid-2026, it effectively leapfrogs TSMC for the first time in a decade. Panther Lake CPUs could reclaim 5-10% of market share from AMD in the laptop segment. Furthermore, a confirmed mega-whale contract from Apple or Qualcomm for foundry services would re-rate Intel from a struggling chipmaker to a critical infrastructure provider, pushing the stock toward the $80 range.

The Bear Case: The Capex Trap to $25

Conversely, if 18A yields stagnate at 60%, Intel remains a high-cost producer. Under this scenario, the current 90% rally is viewed as pricing in perfection. Any delay in the Ohio fab opening or a further $2 billion+ quarterly loss in the foundry unit could trigger a violent liquidation. Technical models suggest a retreat to fill the $30 liquidity gap if the AI PC cycle fails to spark a mass consumer upgrade.

How to Trade Intel Stock Futures with USDT on BingX TradFi

Intel stock perpetuals on the futures market with BingX AI analysis

Maximize your trading precision by leveraging BingX AI to analyze Intel’s 18A yield trends and institutional liquidity zones in real-time.

1. Access the TradFi Market: Log in to BingX and go to the TradFi section under Markets. Select INTC/USDT perpetuals.

2. Monitor the 18A Newsflow: Watch for Risk Production vs. Volume Production headlines. Volume production is the ultimate buy signal for momentum traders.

3. Choose Your Leverage: Intel’s $3–$5 daily swings are common in 2026. Professionals typically use 3x–5x leverage to manage the gap-risk associated with earnings reports.

4. Set Strategic TP/SL: Automate your exit strategy by utilizing BingX’s Take-Profit (TP) and Stop-Loss (SL) orders to shield your collateral from extreme pre-market volatility. Given that semiconductor stocks in 2026 often gap 5% higher or lower at the opening bell due to overnight manufacturing news from Asia, having a pre-set SL in place is the only way to ensure a volatile session doesn't lead to unexpected liquidation.

5 Key Risks for Intel Traders in 2026

Navigating Intel’s high-stakes turnaround requires a firm grasp of the structural hazards unique to the 2026 semiconductor landscape.

1. The Foundry Cash Burn: Intel is spending billions on fabs. If federal CHIPS Act funding is delayed or reduced, the liquidity stress could force a dividend cut or share offering.

2. AMD’s Server Dominance: AMD is targeting 40% of the server market. If Intel's Xeon chips continue to lose ground in the data center, the high-margin cash cow that funds the fabs will die.

3. The Taiwan Strait Premium: Much of Intel's current valuation is a safety premium. If geopolitical tensions ease significantly, some of that onshoring value may rotate back to cheaper Asian stocks.

4. Yield Stagnation: Manufacturing at 1.8nm is incredibly difficult. A minor defect in the EUV (Extreme Ultraviolet) lithography process can ruin thousands of wafers, leading to massive earnings misses.

5. The Leadership Transition: While Lip-Bu Tan is highly respected, any signs of friction between the Board and the C-suite could spook institutional investors who are betting on his specific back-to-basics strategy.

Conclusion: Should You Invest in Intel (INTC) in 2026?

Intel’s 2026 trajectory represents a fundamental shift from a legacy chipmaker to a critical infrastructure provider for the Western world. If the company successfully converts its 18A process node into consistent high-volume yields, the current valuation may appear as an attractive entry point relative to its 2027–2028 earnings potential. However, the investment thesis relies heavily on the National Champion narrative and the successful execution of the independent foundry model, which remains a capital-intensive and high-risk endeavor.

For BingX traders, the near-term strategy revolves around navigating a U-shaped recovery defined by binary manufacturing milestones. Market participants should prioritize agility, focusing on technical validations such as monthly yield improvements and new mega-whale customer commitments. Conversely, any evidence of stagnating fab utilization or foundry losses exceeding $3 billion per quarter could signal a breakdown in the turnaround story, necessitating a pivot toward defensive or short-biased positioning.

Risk Reminder: Semiconductor stocks are highly cyclical and sensitive to interest rates and geopolitical news. The Foundry Premium can evaporate if manufacturing targets are missed. Always utilize stop-loss orders and never over-leverage on a single earnings narrative.

Related Reading

1. Tesla (TSLA) Stock Outlook for 2026: Can the Great AI and Robotaxi Pivot Take TSLA Stock to $600?

2. Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

3. Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?

4. Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?